The Executive Board of the International Monetary Fund (IMF) has concluded its 2024 Article IV Consultation with Vietnam, projecting the country’s economic recovery and growth to reach 6.1 percent in 2024. This positive outlook is underpinned by strong external demand, resilient foreign direct investment (FDI), and accommodative government policies.

According to the IMF report, domestic demand is expected to gradually improve as companies navigate high debt levels, although the real estate sector may take longer to recover fully. Inflation is projected to stay around the State Bank of Vietnam’s target range of 4-4.5 percent this year. The IMF noted that inflationary pressures have increased, primarily driven by rising food prices, while core inflation remains stable.

The report highlights that Vietnam’s external current account posted a significant surplus of 5.8 percent of GDP in 2023, largely due to a contraction in imports. The IMF’s executive directors praised the Vietnamese authorities for their prompt actions to maintain macro-financial stability amid both domestic and external challenges that emerged as the economy recovered from the pandemic.

Despite these commendations, the IMF also pointed out that downside risks remain elevated. A potential weakening of exports, a key economic driver, could occur if global growth falters, geopolitical tensions persist, or trade disputes escalate. Additionally, the report warns that prolonged exchange rate pressures could lead to increased domestic inflation.

The IMF expressed concern that persistent weaknesses in the real estate sector and the corporate bond market could limit banks’ credit expansion, potentially hindering economic growth and financial stability. As a response, the report emphasizes the need for further efforts to bolster macro-financial stability and implement reforms aimed at addressing these vulnerabilities while ensuring robust, green, and inclusive growth over the medium term.

The IMF advocates for fiscal policy to take the lead in supporting economic activity, given the ample fiscal space available and limited opportunities for monetary policy easing. The IMF welcomed the authorities’ plans to expedite public investment implementation, which will require addressing existing bottlenecks, and noted the importance of expanding social safety nets to protect the most vulnerable segments of the population.

In terms of debt, Vietnam’s total external debt is projected to stand at 32.6 percent of the GDP by the end of 2024, with public and publicly guaranteed debt forecasted at 33.8 percent. The IMF noted that the Vietnamese authorities have effectively contained inflation risks, though they cautioned that monetary policy must remain cautious given the complex economic environment.

The report also commended Vietnam’s progress toward greater exchange rate flexibility and encouraged continued efforts to modernize the monetary policy framework. The IMF stressed the importance of strengthening the resilience of the financial system by enhancing capital buffers, phasing out regulatory forbearance, and addressing rising non-performing loans.

Furthermore, the IMF highlighted the need for decisive actions to mitigate risks in the real estate and corporate bond markets, recommending the strengthening of the insolvency framework and increasing transparency within the corporate bond market. The Fund applauded the government’s anti-corruption initiatives and emphasized the importance of ongoing governance improvements.

In its latest update, the IMF revised its GDP growth forecast for Vietnam in 2024 up to 6.1 percent, an increase from the 5.8 percent projected in April. The country’s GDP is expected to reach US$468.5 billion this year and US$506.4 billion next year. Credit to the economy is projected to grow by 12.9 percent in 2024 before slowing to 9.5 percent in 2025, compared to 13.7 percent in 2023.

The IMF anticipates that Vietnam’s gross international reserves will decrease to US$84 billion in 2024 from US$92.3 billion in 2023. The report concludes by reiterating the importance of expediting public investment and strengthening fiscal frameworks to support Vietnam’s ambitious development agenda while fostering economic resilience and inclusivity.

In the first nine months of 2024, Vietnam’s Gross Domestic Product (GDP) increased by 6.82% year-on-year, with a GDP growth rate of 7.4% in the third quarter. The socio-economic situation in the third quarter and the first nine months of the year continues to show positive trends, with various sectors gaining significant achievements, laying a foundation for further growth in the remainder of the year.

Viet Nam’s economic growth is expected to pick up in 2024, driven by a rebound in manufactured exports and tourism, and recovering consumption and business investment, the World Bank said today in a new report.

Viet Nam’s economy is forecast to grow 6.1 percent in 2024, and 6.5 percent in both 2025 and 2026, up from 5 percent last year, according to the Bank’s latest Taking Stock report. The report highlights the resilience of the Vietnamese economy despite rising global challenges.

The report, “Reaching New Heights in Capital Markets,” notes that the economy is not yet back to its pre-pandemic growth path. Enhanced public investment would provide short-term stimulus while also addressing emerging infrastructure gaps – for example in energy, transport, and logistics – which are becoming a growing constraint on growth, the report said. Bank asset quality remains a concern given rising non-performing loans (NPLs) and should be closely monitored by the authorities.

“During the first half of the year, Viet Nam’s economy benefitted from the rebound in export demand,” said World Bank East Asia and Pacific Practice Manager for Macroeconomics, Trade, and Investment Sebastian Eckardt. “To sustain growth momentum not only for the rest of the year but over the medium-term, the authorities should deepen structural reforms, step up public investment while carefully managing emerging financial risks.”

A special chapter of the report finds that development of capital markets would provide a vital source of long-term funding for Viet Nam’s economy and help the country achieve its goal of becoming a high-income nation by 2045. The report highlights key challenges, including underdevelopment of the institutional investor base and underutilization of the Viet Nam Social Security fund (VSS).

The report recommends a stronger policy framework, in which VSS could be a force in driving capital market development. Policies that would allow markets to reclassify Viet Nam from Frontier Market status to Emerging Market status would help attract more foreign investors, as would reforms to enhance market transparency and investor protection. Effective coordination among financial regulators is crucial for achieving these goals.

“Billions of dollars of global investment funds will flow into the capital markets if Viet Nam is upgraded to the Emerging Market status,” said World Bank Senior Financial Sector Specialist Ketut Ariadi Kusuma. “At the same time, gradual diversification of VSS investment is key not only to improve its long-term investment returns, but also to fuel Viet Nam’s economic growth through investments in the corporate sector.”

Taking Stock is the World Bank’s bi-annual economic report on Viet Nam.

Many households will have to wait for some time to feel the benefit of lower interest rates.

The bigger-than-expected cut in interest rates by the United States Federal Reserve may have sent the stock market cheering, but its impact on the economy, and the upcoming presidential election, is mixed, experts say.

The US Fed on Wednesday cut the benchmark federal funds rate by half a percentage point to the 4.75 percent to 5 percent range “in light of the progress on inflation and the balance of risks”, the rate-setting committee said in a statement.

The rate had been in the 5.25 percent to 5.5 percent range since July 2023.

Since then, inflation – which hit a 40-year high of 9.1 percent in mid-2022 – has been inching its way down and is now at 2.5 percent, within spitting distance of the Fed’s target of 2 percent.

While the cut was bigger than expected, most US mortgage holders will see no benefit as more than 90 percent of borrowers have fixed-rate loans.

For households with variable-rate mortgages or student loans, relief will take some time, as the terms of repayment typically reset only once every six months or a year.

Some of the biggest beneficiaries of the rate cut will be prospective homebuyers.

The average rate on a 30-year fixed-rate mortgage last week fell to 6.09 percent from a high of nearly 8 percent last October, according to Freddie Mac, fuelled by expectations of lower interest rates.

“The Fed was more aggressive than we expected and that might translate into mortgage rates coming down a bit more as more cuts are due later in the year,” Nancy Vanden Houten, lead economist at Oxford Economics, told Al Jazeera.

Still, while mortgage rates are dropping, “the cut is unlikely to address other drivers of affordability in housing which reflect lower supply, and in fact some asset owners, hoping for lower interest rates to spark investment, may actually raise their expectations of price for those assets”, said Rachel Ziemba, an economist and founder of Ziemba Insights.

On other fronts, interest rates on auto loans and credit card loans are expected to come down.

But since rates are currently above 8 percent for five-year car loans, and more than 21 percent for credit cards, as per Fed data cited by the Reuters news agency, any savings are likely to be modest.

‘Policy uncertainty’

Analysts offered mixed assessments of how the rate cut may affect voter sentiment for the November 5 presidential election.

“This will be a net positive for [Democrat presidential nominee] Kamala Harris,” said Vanden Houten, adding that the rate cut should “guard against any further weakening” of the economy, particularly in the labour market.

“We have already seen a boost in consumer confidence on the expectations of a cut. This is a very close election and polls still show voters give [Republican presidential nominee Donald] Trump an edge on the economy, but this still helps Vice President Harris,” she said.

Ziemba was not so sure.

While the economic effects of the cut will not be fully apparent for months, the candidates are likely to put different spins on the Fed’s decision in the lead-up to the election, Ziemba said.

“The Democrats may point to the Fed’s signal that the economy is doing OK, the Republicans may claim that the Fed is trying to play catchup and benefit their rivals. Ultimately, other perceptions of economic policy will likely be more important, including food and fuel prices, as well as other costs like rising health insurance which won’t be reduced by rate cuts,” she said.

Ziemba said the “policy uncertainty” raised by the election outcome, including the prospect of sweeping tariffs under a second Trump presidency, may overshadow the impact of any decisions by the Fed.

“The uncertainty about fiscal and trade policy can undermine benefits from lower interest rates,” Ziemba said.

As 2025 approaches, Capital Economics analysts said in a note this week that they expect a modest recovery for most major global economies following a challenging second half of 2024.

According to the firm’s analysis, two key themes will shape advanced economies: the normalization of inflation and the loosening of monetary policy, “both of which should offer some support to GDP growth,” said the firm.

Additionally, China’s recovery is expected to pick up as fiscal stimulus takes effect, although ongoing trade tensions with the U.S. and its allies may limit its growth potential.

However, several risks remain on the horizon, according to Capital Economics. The firm highlights the “stickiness of inflation, especially in Europe,” which could hinder real income growth and reduce the scope for policy easing.

Moreover, political transitions in various countries are said to pose uncertainties, with potential risks around debt-funded stimulus and financial market reactions.

The firm believes the rise of isolationist trade policies and stronger pushback against immigration are also flagged as concerns, potentially leading to stagflationary effects in advanced markets.

While some fear that recession is on the horizon for 2025, Capital Economics remains cautiously optimistic.

They note warning signs such as a downturn in manufacturing surveys, rising unemployment, and increasing loan delinquencies, but emphasize that these indicators alone don’t guarantee a recession.

“Trends in credit, employment, retail sales, and construction still paint a broadly positive picture,” said Capital Economics.

Overall, they predict that a “soft landing is the most likely outcome” for 2025, though they are closely monitoring the evolving risks.

Recent forecasts are optimistic about the Vietnamese economy in 2024 with the gross domestic product (GDP) growth rate poised to reach around 7 per cent for the full year, higher than the National Assembly’s target set at 6.5 per cent.

The Central Institute for Economic Management (CIEM) on Tuesday lifted its growth forecast for the Vietnamese economy from 6.48 per cent to 6.95 per cent, in the context of a robust global economic recovery.

CIEM’s Director Nguyễn Hồng Minh said at a conference discussing new drivers for quality growth, that Việt Nam’s socio-economic development achieved impressive results in the first half of this year, prioritising stabilising the macroeconomy, controlling inflation and ensuring major balances.

GDP expanded at 6.42 per cent in January-June, inflation was under control, exports and inflows of foreign direct investment (FDI) were robust. “More important, Việt Nam is considered a spotlight of reform and economic integration,” Minh said.

“Economic restructuring, regional economic development, improving business environment, enhancing labour productivity together with digital and green transitions are becoming bold policies.”

Nguyễn Anh Dương, Head of the CIEM’s General Research Department, said that the prospect of Việt Nam’s economic growth was positive compared to other countries in the region.

The CIEM has provided two scenarios for GDP growth in 2024.

In the first scenario, GDP growth is forecast to reach 6.55 per cent in 2024 with exports to increase by 9.54 per cent, CPI at 4.31 per cent and trade balance to record a surplus of US$5.7 billion.

Dương said that the first scenario was built on the context the global economy develops following projections of international organisations and Việt Nam maintains similar policies as in the first half of the year.

In the second scenario, GDP growth can reach 6.95 per cent if the global economy sees more rapid recovery, internationals increase investments in Southeast Asia, including Việt Nam and investments in digital and green transitions see positive developments. In this context, exports will increase by 11.64 per cent over 2023, CPI at 4.12 per cent and trade surplus at $7.3 billion.

“To reach the GDP growth rate of 6.95 per cent, Việt Nam needs to effectively implement reforms and economic management policies to maximise the efficiency of public investment disbursement and credit absorption, improve labour productivity, enhance business environment and the national competitiveness, Dương said.

Greater efforts should be made to increase the quality of growth, the capacity of innovation and adaptation to major trends such as digital transformation and green transition, enhance labour productivity and complete the legal framework for new economic models like circular economy, digital economy, sharing economy and innovative economy, he said.

Adding that close watch must be kept on inflation developments, especially impacts of wage increases and price increases of State-managed products, to maintain room for fiscal policies in case there are external shocks.

Bike production at Thống Nhất Company Limited. Recent forecasts are optimistic about the Vietnamese economy in 2024 with the gross domestic product (GDP) growth rate poised to reach around 7 per cent for the full year. — VNA/VNS Photo Trần Việt

7% GDP growth target?

After impressive economic growth in the first half of this year, the Ministry of Planning and Investment recently proposed to the Government a growth scenario for the full year to 6.5-7 per cent, instead of 6-6.5 per cent target set in the Government’s Resolution No 01.

The ministry raised two growth scenarios with GDP to reach 6.5 per cent and 7 per cent, respectively.

The ministry boldly proposed the Government strive for the target of 7 per cent or higher on positive growths of economic sectors, more rapid recovery of private investment, State-owned enterprises, positive growth momentum of foreign direct investment (FDI), robust exports, improving tourism and consumption and new policies, urging more drastic policies.

Minister of Planning and Investment Nguyễn Chí Dũng said that the early enforcement of the Law on Land, Law on Real Estate Business and Law on Housing would create favourable conditions for the property market to recover in the second half of this year, which would positively affect economic growth.

Meanwhile, most international organisations’ projections put the expansion of the Vietnamese economy at around 6 per cent this year.

According to José Viñals, group chairman of Standard Chartered, the Vietnamese economy will perform better this year to reach a GDP growth rate of 6 per cent in the second half, leading to an overall yearly rate of 6 per cent.

“Relative to most other economies, a 6 per cent growth rate is quite impressive, nearly double the global rate and higher than emerging markets, which are expected to grow around 4 per cent this year. This places Việt Nam among the top growth economies globally, which is something to be happy about,” he said.

The Singaporean-based United Overseas Bank (UOB)’s Global Economics & Market Research Unit earlier this month maintained its growth forecast for Việt Nam at 6 per cent for 2024.

The International Monetary Fund (IMF) projects the Vietnamese economy to expand by close to 6 per cent in 2024, driven by a recovering export sector, robust foreign direct investment and policy support.

However, downside risks are high, the IMF warned.

“Exports, a key driver for Việt Nam’s economy, could weaken if global growth disappoints, global geopolitical tensions persist, or trade disputes intensify. Domestically, persistent weakness in the real estate sector and corporate bond market could weigh more than expected on banks’ ability to expand credit and hurt economic growth and undermine financial stability. Given easy monetary conditions, if exchange rate pressures were to persist for longer it could lead to a larger pass-through to domestic inflation,” the IMF wrote.

To sustain high economic growth amid less-favorable demographics and climate change challenges, Việt Nam needs a new wave of reforms, according to the IMF.

“Increasing productivity, further investing in human and physical capital and incentivising private investment in renewable energy is key. Improving the functioning of the capital markets would also help boost productivity. In this regard, developing a market-based sovereign bond market is vital to facilitate broader capital market development and to make monetary policy transmission more effective.”

Vietnam showcased strong performances across multiple indicators in the first half of 2024, prompting the General Statistics Office (GSO) to project a 6-6.5 percent growth rate for the year, aligning with the government’s target.

According to the GSO, Vietnam experienced a 6.42 percent growth in gross domestic product (GDP) year-on-year in H1 2024, slightly lower than the 6.58 percent reported during the same period in 2022. The GSO attributed Vietnam’s strong economic performance to the resilience of the global economy despite uncertainties and volatilities.

Below we discuss Vietnam’s economic data for H1 2024 and growth projections to the end of the year.

Vietnam GDP and growth projections for 2024.

The United Overseas Bank (UOB), The Asian Development Bank, Standard Chartered, and HSBC have all maintained their growth forecasts for Vietnam at 6 percent for 2024. In June, a team from the International Monetary Fund (IMF) led by Paulo Medas noted that Vietnam’s economy had rebounded and grew by 6.4 percent year-on-year in H1.

Meanwhile, in a July ASEAN+3 regional outlook report, AMRO revised its GDP growth forecast for Vietnam upward to 6.3 percent from 6 percent in its April report while maintaining a 6.5 percent increase for the 2025 projection.

During the government’s regular press briefing in Hanoi on July 6, Deputy Minister of Planning and Investment Tran Quoc Phuong stated that registered foreign direct investment (FDI) is expected to reach US$40 billion this year.

The Central Institute for Economic Management (CIEM), under the Ministry of Planning and Investment (MPI), recently reported that real GDP growth had exceeded its potential for four consecutive quarters. CIEM projected two scenarios for this year’s GDP growth:

In the normal scenario, GDP is expected to reach 6.55 percent, inflation at 4.32 percent, and export growth at 9.54 percent.

In a more positive scenario, GDP could expand by nearly 7 percent, with average inflation lower at 4.12 percent, and export growth exceeding 11.64 percent.

Investments

FDI

According to the GSO, FDI inflows into Vietnam reached nearly US$15.2 billion during the first six months of 2024, marking a 13.1 percent annual increase.

As of June 20, 2024, foreign investors had registered about US$9.54 billion in 1,538 new projects, reflecting a 47 percent rise in capital and a 19 percent increase in the number of projects compared to last year. Additionally, they spent US$3.95 billion in additional capital and US$1.698 billion on capital contributions and share purchases.

During the same period, Vietnam recorded US$10.842 billion in disbursed capital, an 8.2 percent annual increase and the highest record over the past five years.

In terms of investment by countries/regions, Singapore led the list of Vietnam’s most prominent investors with a total capital of US$5.579 billion, accounting for 36.74 percent of the total FDI inflow. Japan followed in second place with US$1.731 billion, representing 11.399 percent of the total. Hong Kong (China) was close behind with US$1.730 billion in investments, making up 11.393 percent. South Korea and China followed with investments of US$1.411 billion and US$1.299 billion, respectively, contributing 9.292 percent and 8.554 percent.

Public investments

Experts have observed stagnation in the disbursement of public investment funds. Allocated capital remains idle, with several ministries and departments yet to disburse their funds. Further, total public investment resources in 2024 are already lower than last year.

Vietnam had one IPO in H1 2024

According to global consultancy Deloitte, Vietnam had only one initial public offering (IPO) in the first half of this year. DNSE Securities JSC listed on the Ho Chi Minh Stock Exchange (HoSE), raising US$36.9 million for an IPO market capitalization of US$135 million. This single listing surpassed the market performance of the three IPOs in 2023, which collectively raised around US$7 million.

Vietnam’s new stock trading system, KRX, is scheduled to launch in September 2024, a delay from the initial plan.

Trade

From January to June 2024, Vietnam recorded export revenues of US$190.08 billion, a 14.5 percent increase year-on-year, while import expenditures rose 17 percent to US$178.45 billion. This resulted in a trade surplus of US$11.63 billion, lower than the US$13.4 billion recorded in the first half of 2023.

In particular, the FDI sector posted export revenues of US$136.69 billion, increasing 12.3 percent year-over-year, while import expenditures rose 14.1 percent to US$112.71 billion, resulting in a US$23.98 billion trade surplus.

Conversely, the domestic sector experienced a US$12.35 billion trade deficit.

Vietnam’s Key Export and Import Sectors in H1 2024

Categories

Values(US$ billion)

Performance compared to 2023 (%)

Export

Electronics, computers, and components

32.91

28.6

Phones and components

22.2

11.3

Machinery and equipment

22.93

16.2

Apparel and textiles

16.28

3.1

Footwear

10.84

10

Import

Electronics, computers, and components

48.84

26.7

Phones and components

22.31

14.6

Machinery and equipment

7.12

10.8

Apparel and textiles

5.05

24

Footwear

5.36

14.7

–

Vietnam’s Export Revenue and Import Expenditure in H1 2024

Categories

Values (US$ billion)

Performance compared to 2023 (%)

Export revenue

Manufacturing and processing

166.79

87.7

Farm produce and forestry goods

16.64

8.8

Fisheries

4.36

2.3

Fuel and natural resources

2.29

1.2

Import expenditure

Materials for production

167.73

94

Consumer goods

10.72

6

Key trade partners

China was Vietnam’s biggest trade partner in H1 2024, with a total trade value of US$94.8 billion, followed by the U.S. at US$61.4 billion and the ASEAN bloc at US$40.8 billion. China was also Vietnam’s largest import market, while the U.S. was its most prominent export destination.

Specifically, Vietnam spent US$67 billion on imports from China, a 34.7 percent year-over-year increase, and earned US$27.8 billion from exports to China, a 5.3 percent increase.

Vietnam’s exports to the U.S. rose 22.1 percent year-over-year to US$54.3 billion, while imports from the U.S. increased by 2.8 percent to US$7.1 billion.

Other major trade partners of Vietnam included South Korea, the EU, and Japan, with total trade values reaching US$38.4 billion, US$32 billion, and US$21.7 billion, respectively.

Industries

The added value of industrial production grew by 7.54 percent from the first half of 2023 to the same period this year.

The manufacturing and processing sector remained the primary driver of overall economic growth. The S&P Global Vietnam Manufacturing Purchasing Manager’s Index (PMI) surged to 54.7 in June 2024 from 50.3 a month earlier, signaling strengthened business conditions and marking a third consecutive month of growth.

Simultaneously, the GSO reported that 56 industries recorded an increase in the Industrial Production Index (IIP), although seven industries experienced otherwise. In a separate report dated June 19, the World Bank (WB) noted a 2.6 percent month-on-month increase in Vietnam’s IIP for May.

However, the surge in new orders created immense pressure on operating capacity, causing workloads to pile up more noticeably for the second time in three months.

Meanwhile, statistics indicate that growth rates in specific service sectors, including wholesale and retail, automobile and motorcycle repair, and finance and banking, were less robust compared to H1 2023.

Employment

The GSO estimated Vietnam’s unemployment rate was 2.27 percent in the first six months of 2024, consistent with the same period last year. The agency also assessed the urban and rural unemployment rates to be at 2.68 and 2 percent, respectively.

The unemployment rate among the 15-to-24 age group is estimated to have risen to 8 percent, an increase of 0.49 percentage points from H1 2023. The annual rate for 2024 is estimated to be 8.02 percent in 2024, an increase of 0.6 percentage points from the previous year.

As of the end of June, Vietnam’s workforce aged 15 and above is estimated at 52.5 million people, up 196,600 year-on-year. This figure includes 27.86 million males and 24.6 million females, with increases of 110,100 and 86,500 year-on-year, respectively. Approximately 51.4 million people aged 15 or older were employed in H1 2024.

The service sectors dominated the country’s workforce, employing 20.7 million workers (40.2 percent), followed by industry and construction with 17 million (33.1 percent), and agriculture-forestry-fisheries with 13.7 million (26.7 percent).

Labor income

According to the GSO, in H1 2024, the average monthly income of contracted workers was approximately VND7.5 million (US$295), which increased by VND519,000 (US$20.4) year-on-year.

Vietnamese male workers with labor contracts earned an average monthly income of VND8.5 million (US$334), while their female counterparts earned about VND6.4 million (US$251.4). In urban areas, the average monthly income was VND9.1 million (US$357), whereas in rural areas, it was VND6.5 million (US$255).

Inflation

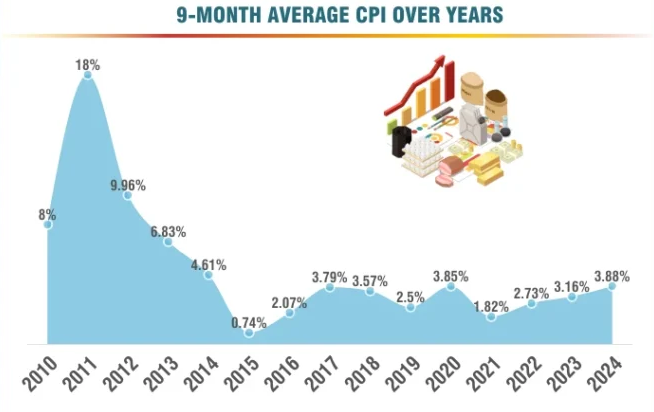

Experts highlight that Vietnam’s economy is facing significant pressure, particularly evident in several key macroeconomic indicators, with inflation being particularly noteworthy. Core inflation rose by 2.75 percent, while the average Consumer Price Index (CPI) increased by 4.08 percent in H1 2024 compared to the same period last year, surpassing the lower end of the annual target range of 4-4.5 percent. The CPI has shown a consistent monthly upward trend.

Inflation is expected to continue rising due to supply fluctuations, global price volatility, and increased demand for electricity and services like transportation and tourism during the peak summer season. Wage increases that took effect from July 1, along with anticipated adjustments in prices of state-controlled items such as electricity, medical services, and education, are also likely contributors to inflationary pressures.

Domestic consumption has shown some improvement but has fallen short of expectations. The total value of retail sales and consumer service revenue (excluding price factors) increased by only 5.7 percent over the past six months, significantly below anticipated levels.

What businesses should pay attention to

Despite positive developments across various aspects, Vietnam’s economy faces latent risks that could impact businesses adversely. These include potential currency depreciation and the recent rise in public wages, necessitating vigilant oversight and responsive measures from the State Bank of Vietnam (SBV) to manage these risks effectively.

Enterprises also encounter ongoing challenges such as persistent issues in the business environment, constraints in accessing capital, and elevated input costs amid a competitive output market landscape.

Experts recommend that businesses and industries take proactive measures to mitigate potential negative impacts:

Monitor production and business conditions closely to preempt emerging risks. This involves advocating for policies that remove barriers and allocate resources effectively to businesses and production facilities, particularly in processing, manufacturing, and market services.

Strengthen linkages between production and distribution channels. This approach would benefit from efficient public investment disbursement, crucial for meeting targets and supporting other economic sectors.

Innovate trade promotion strategies to leverage market recovery trends and capitalize on export opportunities.

The National Assembly has extended a 2 percent reduction in value-added tax (VAT) on selected goods and services until the year’s end to stimulate demand. Some proponents advocate extending this policy until the end of 2025 and implementing deeper VAT cuts to further encourage consumer spending.